Tutorial interpolation¶

[1]:

import matplotlib.pyplot as plt

import numpy as np

[2]:

from ropwr import RobustPWRegression

Basic¶

This tutorial shows the capabilities of the robust piecewise regression class to be used as an interpolator. Two well-known application in quantitative finance, the interpolation of yield curves and probability default curves, will serve as examples.

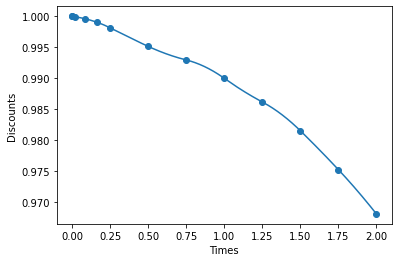

First, we are interested in interpolating a discount curve given by a set of discount factors and maturities. To simplify the problem, we use times instead of maturities. This example is presented in https://www.quantlib.org/slides/dima-ql-intro-2.pdf (slide 90).

[3]:

times = np.array([0.0, 1/365, 1/52, 1/12, 2/12, 3/12, 6/12, 9/12, 1, 5/4, 6/4, 7/4, 2])

discounts = np.array([1.0000000, 0.9999656, 0.9999072, 0.9996074, 0.9990040,

0.9981237, 0.9951358, 0.9929456, 0.9899849, 0.9861596,

0.9815178, 0.9752363, 0.9680804])

plt.scatter(times, discounts)

plt.xlabel('Times')

plt.ylabel('Discounts')

plt.show()

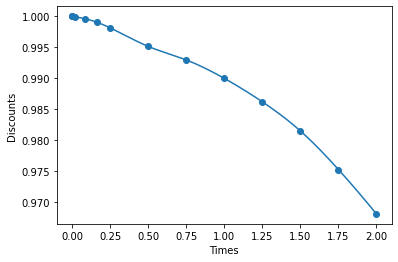

Note that interpolation requires the regression funtion \(f\) at the known points \((x_i, y_i)\) to satisfy \(f(x_i) = y_i\). Therefore, splits points must be \(x_i\), \(i=1,\ldots, n\). Also, note that the default parameter continuous_deriv=True results in spline interpolation.

We generate a time space to calculate interpolated values.

[4]:

time_space = np.linspace(1/365, 2, 1000)

[5]:

pw = RobustPWRegression(degree=2, monotonic_trend="descending", solver="ecos")

pw.fit(times, discounts, splits=times)

plt.scatter(times, discounts)

plt.plot(time_space, pw.predict(time_space))

plt.xlabel('Times')

plt.ylabel('Discounts')

plt.show()

Check interpolated values at split points (known data points).

[6]:

pw.predict(times)

[6]:

array([1. , 0.9999656, 0.9999072, 0.9996074, 0.999004 , 0.9981237,

0.9951358, 0.9929456, 0.9899849, 0.9861596, 0.9815178, 0.9752363,

0.9680804])

To interpolate in the rates, it is common to apply a logarithmic transformation on the discount curve. The perform this transformation, set space="log".

[7]:

pw = RobustPWRegression(degree=3, solver="osqp", space="log")

pw.fit(times, discounts, splits=times)

plt.scatter(times, discounts)

plt.plot(time_space, pw.predict(time_space))

plt.xlabel('Times')

plt.ylabel('Discounts')

plt.show()

Extrapolation¶

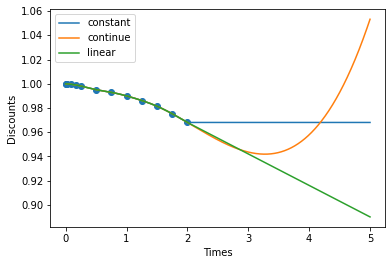

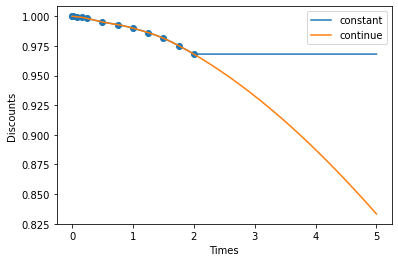

In many applications, we want to extrapolate outside the known points data range. RoPWR introduced extrapolation parameters extrapolation and extrapolation_bounds in version 1.0.0.

Discount curve¶

We generate an extended time space. When space="linear" (default) four extrapolation methods are available:

None: raise exception if value outside \((min(x_i), max(x_i))\)

“constant”: the value of the regression at \((min(x_i), max(x_i))\) is used for constant extrapolation.

“continue”: the regression is extrapolated as is.

“linear”: the regression is linearly extrapolated using the derivatives at \((min(x_i), max(x_i))\).

[8]:

time_space = np.linspace(0, 5, 1000)

[9]:

for extrapolation in ("constant", "continue", "linear"):

pw = RobustPWRegression(degree=3, monotonic_trend="descending", solver="osqp",

extrapolation=extrapolation)

pw.fit(times, discounts, splits=times)

plt.plot(time_space, pw.predict(time_space), label=f"{extrapolation}")

plt.scatter(times, discounts)

plt.xlabel('Times')

plt.ylabel('Discounts')

plt.legend()

plt.show()

Extrapolation might return unexpected results, especially as the degree increases. For this particular case, we can improve the results using log-space.

[10]:

for extrapolation in ("constant", "continue"):

pw = RobustPWRegression(degree=3, monotonic_trend="descending", solver="osqp",

extrapolation=extrapolation, space="log")

pw.fit(times, discounts, splits=times)

plt.plot(time_space, pw.predict(time_space), label=f"{extrapolation}")

plt.scatter(times, discounts)

plt.xlabel('Times')

plt.ylabel('Discounts')

plt.legend()

plt.show()

Probability default curve¶

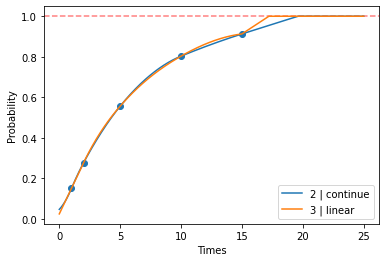

In this section example, we create a probability default curve with 15% deterministic one-year probability of default.

[11]:

times = np.array([1, 2, 5, 10, 15])

probs = 1 - (1 - 0.15) ** times

time_space = np.linspace(0, 25, 1000)

We set the maximum value to 1 (100% probability) using extrapolation_bounds. If the extrapolated values hit the bounds, constant extrapolation is applied from the intersection points onward.

[12]:

plt.scatter(times, probs)

plt.axhline(y=1, color='r', linestyle='--', alpha=0.5)

for degree, extrapolation in ((2, "continue"), (3, "linear")):

pw = RobustPWRegression(degree=degree, monotonic_trend="ascending", solver="osqp",

extrapolation=extrapolation, extrapolation_bounds=(0, 1))

pw.fit(times, probs, splits=times)

plt.plot(time_space, pw.predict(time_space), label=f'{degree} | {extrapolation}')

plt.xlabel('Times')

plt.ylabel('Probability')

plt.legend()

plt.show()